The federal government has introduced changes to the rules that govern eligibility for the Age Pension. These rules will take effect on 1 January 2017.

Eligibility to receive the Age Pension depends on how much income you earn from certain other sources (such as interest on savings) and the value of your assessable assets.

These changes apply only to the asset test – there will be no changes to the income test.

Who is affected?

There is no ‘grandfathering’ clause and all Australians currently receiving a full or part pension will be reassessed. The government has indicated that at least 326,000 existing pension recipients will lose all or part of their current pension benefit. However, some part age pensioners may receive an increase.

Any Australian retiring after 1 January 2017 will automatically be assessed under the new thresholds.

Does it affect my home?

The family home continues to be exempt from the Asset Test.

How will it work?

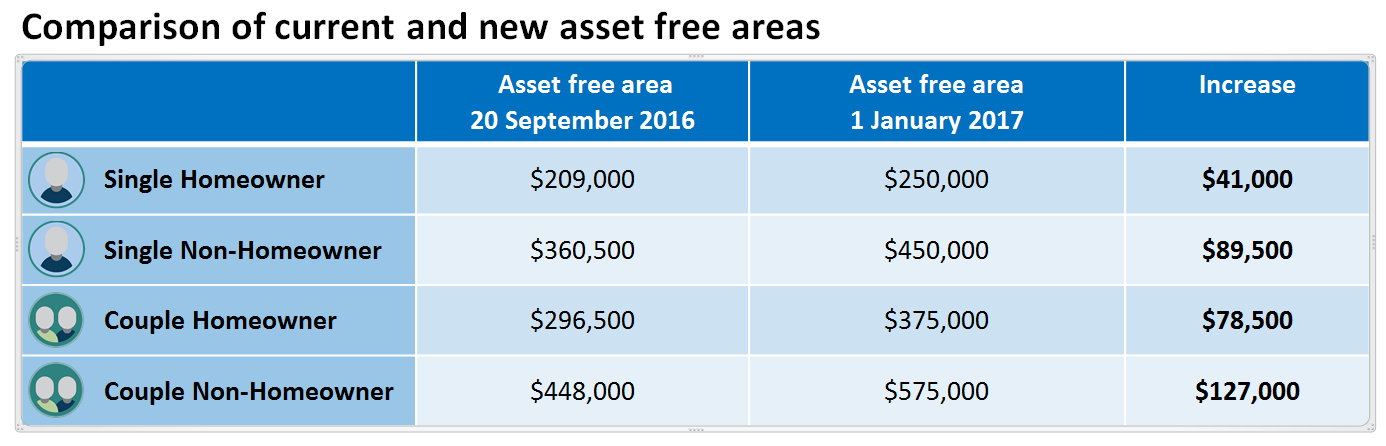

Your assets don’t affect your payment if they are below the assets test free area. The table below sets out the new assets free area. For those people who currently lose some pension this change may result in an increase in your payment.

a) LowerAsset Test Thresholds^

b) The withdrawal rate (or taper rate) is changed

Currently, for every $1,000 of assets you own above the asset free area, your pension reduces by $1.50 per fortnight. From 1 January 2017, for every $1,000 over the asset free area, your pension will reduce by $3.00 per fortnight. This means the amount of assets a pensioner can have on top of their family home and still receive a part pension will be reduced.

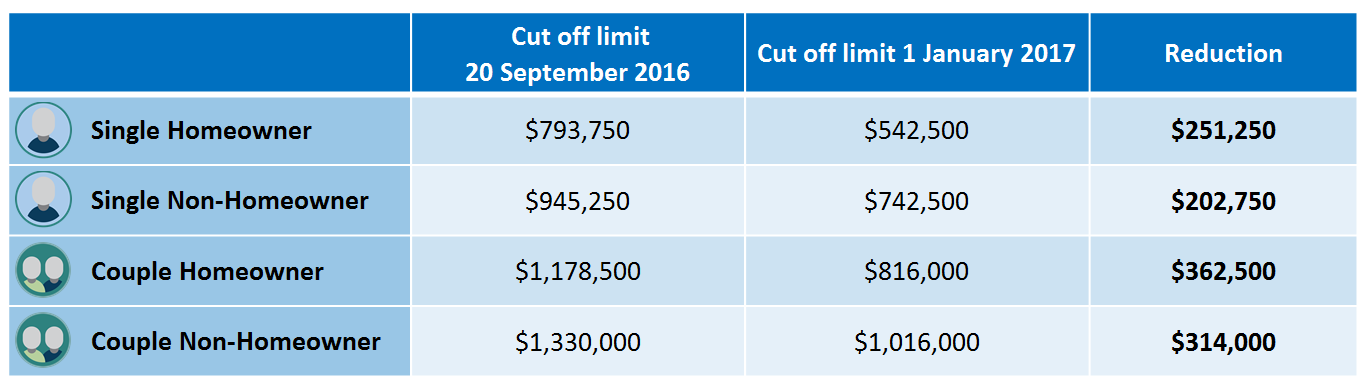

c) Asset Test ‘Cut-Off’ Thresholds^

When the value of your assets reach the maximum cut off, you will lose all entitlements.

Application to other payments

The changed Asset Test rules also apply to other government benefits including:

- Disability support pension

- Wife pension

- Carer payment

- Bereavement allowance, and

- Widow B pension and certain pensions administered by the Department of Veterans’ Affairs.

Additional comments in the legislation indicate that the new Asset Test will also apply to:

- Parenting payment and,

- Allowances (widow allowance, youth allowance, Austudy payment, Newstart allowance, sickness allowance, special benefit and partner allowance)

There has never been a better time to talk to an expert

Talking with a financial expert should not be the last thing you do before retirement, nor should being retired be a reason to not talk with a financial expert.

A financial planner will work with you to help you achieve your financial goals – now and in retirement. The earlier you start, the easier those goals may be to achieve. If you are unsure of how these changes will impact your current age pension entitlements or your future retirement plans, it may be time to talk to a financial planning expert.

Do you know someone who is retired? – Why not pass this information onto a family member or friend who is retired or nearing retirement.

Most industry super funds now offer in house financial planning services. Call them to speak to a financial planner, or contact Industry Fund Services Financial Planning on 1300 138 848.

^ Source: https://www.humanservices.gov.au/customer/enablers/assets#assetstestlimits. Accessed 5 October 2016

This article is issued by Industry Fund Services ABN AFSL (IFS). IFS is one of the largest providers of financial services and products to industry super funds, their members and to unions. The information in this article is general in nature and does not take into account any person’s objectives, financial situation or needs. IFS recommends that before investing in any product you read the Product Disclosure Statement (PDS) and consider its appropriateness for you taking into account your objectives, financial situation and needs.

SHARE:

Age Pension Eligibility – what you need to know