A Historic Bond Rout

With COVID-19 challenging all aspects of our lives, everything is and feels historic. Against this backdrop, non-professional investors can be forgiven for missing the momentous events that took place in the bond market this first quarter (Q1) of 2021.

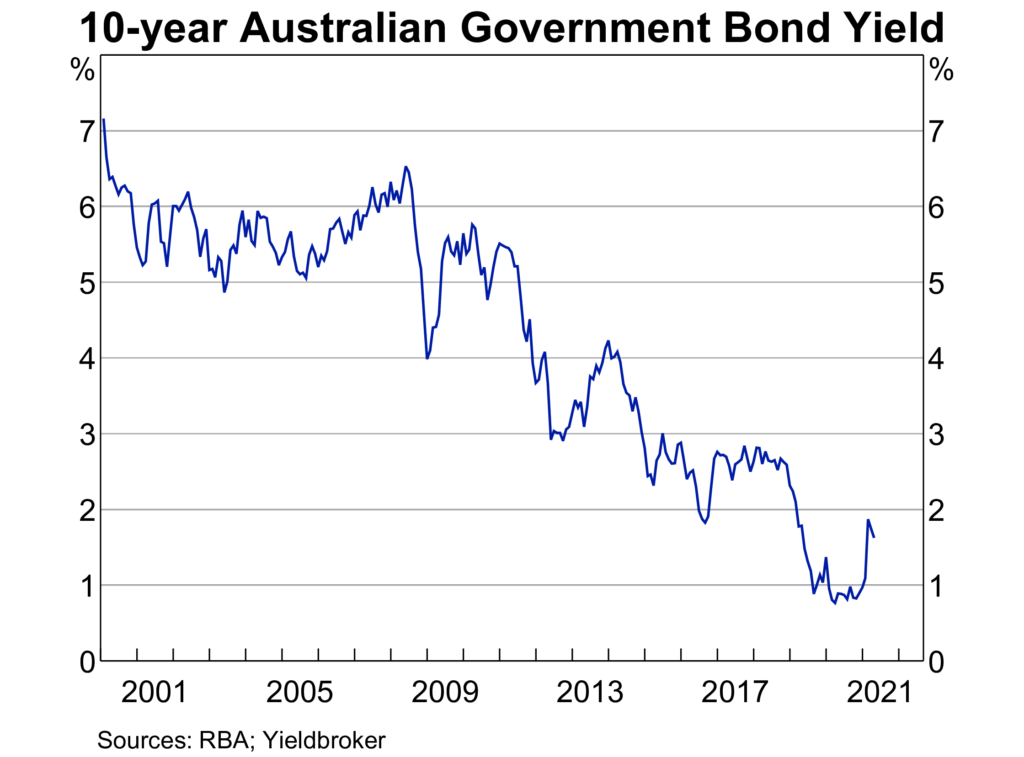

In Q1 of this year, investors sold bonds and interest rates rose at a record pace. In fact, the month of February saw the yield of the 10-year Australian Government Bond rise by nearly 80 basis points or almost 1 per cent. The fastest monthly rise in Australian 10-year interest rates since 1994.

The reason for this mighty move in interest rates was both local and global. Here in Australia, strong economic data indicated that the Australian economy may be growing at a pace that could lead to inflation above the RBA’s target level. And abroad, the scale of the Biden administration’s fiscal stimulus package led many to believe that run-away inflation might be a consequence of unprecedented government largesse.

Taken together, these twin spectres of strong economic growth and the potential for inflation culminated in the large moves we saw in the bond market over the last quarter.

Consequences for Income Investors – The Dog that Didn’t Bark

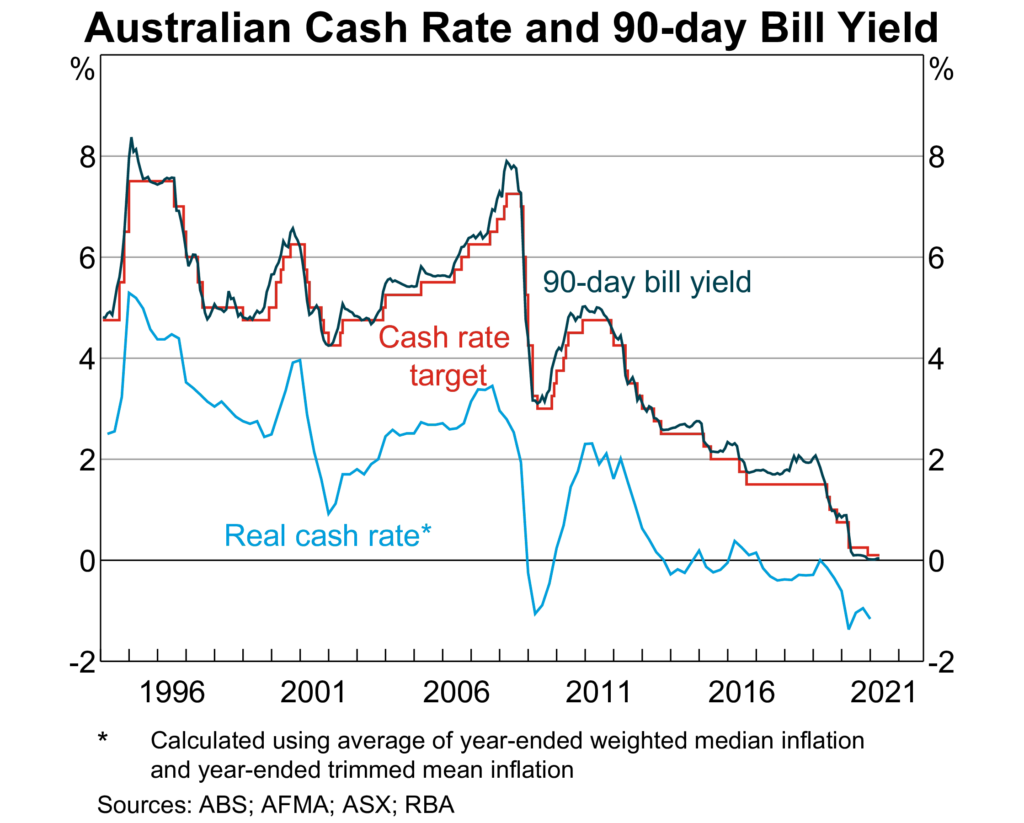

For income investors, equally noteworthy as the interest rates that did rise are those that did not. During most normal economic times, a rise in interest rates like the one we witnessed last quarter would also elicit a corresponding rise in short-term interest rates and thereby the ability of investors to earn income from term deposits. However, because the RBA is effectively controlling the near-term part of the interest rate curve, it has not risen in tandem with long-term fixed income instruments. The RBA’s cash-rate and most term deposits are still at or near zero.

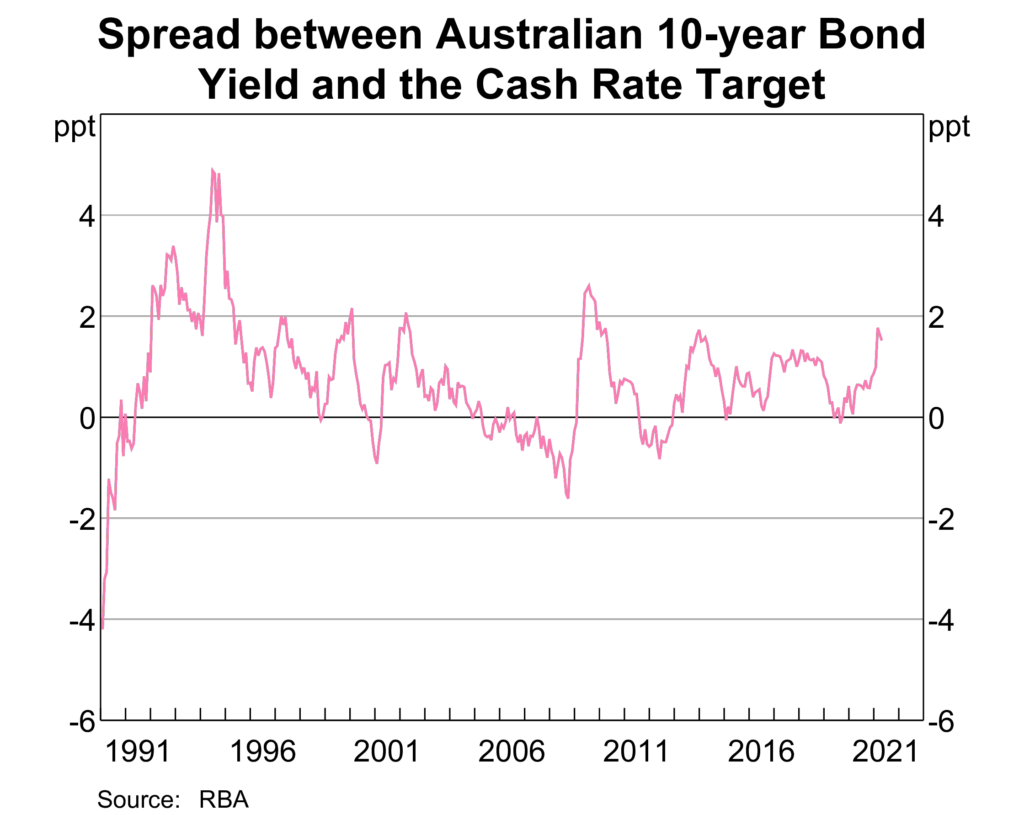

A consequence of this relative performance is – in the parlance of fixed income markets – that the interest rate curve has become even more steep. A steeper curve means that investors have become more incentivized to extend the maturity of their fixed income holdings in order to generate more income or yield.

What to Do Now?

Investors looking for income and yield now face a choice; should they jump into the deep-end and invest into longer-dated bonds to earn more yield or remain in shorter-dated bonds and accept the shallower income streams they offer? The answer, unfortunately, is not as simple as it may first appear.

Extending the maturity of your fixed income holdings, while often generating more yield, also exposes you to the risks of inflation. Case in point, investors who held long-term bonds during the first quarter of 2021 would have experienced volatility and some capital losses (at least on paper).

For most investors, the right answer is to create a diversified portfolio of both short and long maturity fixed income instruments. On our Partnervest platform, we offer diversified model portfolios with range of fixed income exposures so you can choose the portfolio that’s right for you.

With such a portfolio*, you can create rules-based approaches to rebalancing when markets recalibrate as they did earlier this year. This can allow you to adjust your fixed income exposure on your terms, and without betting the ranch or pulling out your hair.

IMPORTANT INFORMATION

*We advise you seek external financial advice before making any investment.

partnervest is a division of Legg Mason Asset Management Australia Limited (Legg Mason Australia), ABN 76 004 835 849, AFSL No. 240827. Legg Mason Australia is part of Franklin Resources, Inc. Before making an investment decision you should read the Product Disclosure Statement (PDS) for the Fund carefully and you need to consider, with or without the assistance of a financial advisor, whether such an investment is appropriate in light of your particular investment needs, objectives and financial circumstances.

SHARE:

What Does a Historic Bond Market Rout Mean for Investors?